Q&A: What is an FHA Loan? How Do I Apply for One?

Read our most important home buying updates for 2024:

What is an FHA loan, and how do I apply for one? These are consistently two of the most frequently asked questions among our readers. The FHA loan program is by far the most popular topic in the mortgage world, especially among first-time home buyers. In this tutorial, you will learn how these loans work and what it takes to qualify for one.

If you're ready to apply for the program, you can use the link provided below. Otherwise, keep reading to learn how this financing program works.

What is an FHA Home Loan?

So what is an FHA loan, exactly? Here is a basic definition, followed by a more thorough examination of the Federal Housing Administration and its mission.

Definition: An FHA home loan is a mortgage that is insured by the federal government, through the Federal Housing Administration. This insurance protects the mortgage lender who makes the loan against losses resulting from borrower default, or failure to pay. The program is managed and overseen by the Department of Housing and Urban Development (HUD). While the program has been around since the 1930s, it has become increasingly popular over the last few years.

The HUD 203(b) Mortgage Insurance program, commonly known as the FHA loan program, offers a path to homeownership for people who might not qualify for a conventional mortgage. (A conventional mortgage loan is one that is not insured by the federal government. Learn more here.) In order to apply for this program, you will have to work with a HUD-approved lender. These are lending institutions that have been approved by the Federal Housing Administration to participate in the program and to offer FHA financing to borrowers.

That answers the first question: What is an FHA loan? Let's talk a little more about how this program works. After that, we will move on to discuss the application process.

The Federal Housing Administration

The Federal Housing Administration (FHA) is a governmental agency that falls under the Department of Housing and Urban Development. The FHA was created with the passing of the National Housing Act in 1934. The date is noteworthy. This new agency was created during the Great Depression, at a time when the mortgage-lending industry was drying up. The FHA's original mission was to make home loans available to a larger number of Americans, primarily by giving lenders an added layer of protection and insurance.

Though the agency's mission has expanded over the years, it is still heavily involved in the mortgage industry. During the first quarter of 2012, this loan program accounted for roughly 30% of all home purchase loans. By way of comparison, in 2005 it accounted for only 4.5% of purchase mortgages. This is an indication of the rising popularity of FHA loans over the last few years in particular.

It is HUD that sets all of the guidelines for this program. These guidelines trickle down through the FHA and all of the individual lenders that participate in the program. The lenders may impose their own guidelines as well, and these requirements can be even stricter than those established by HUD. The industry term for this is an 'overlay.' You'll hear that term again.

Recap: What is an FHA loan? It's a type of mortgage that receives government backing. The government does not lend money directly to borrowers. This is a common misconception. Rather, they insure the loans made by lenders in the private sector. Here's a diagram that shows the relationship between the three parties involved in the process.

As you can see from the illustration above, you apply for this program through a 'regular lender.' That is, a mortgage lender that operates in the private sector. The loan is insured by the federal government, under the direction of HUD and FHA. If the homeowner defaults on the mortgage for any reason, the lender will be compensated for losses (as long as they have made the loan in accordance with HUD's guidelines). The illustration also shows some of the basic requirements for getting an FHA loan. You can learn more about those requirements in this article.

This diagram also gives you some idea of what you'll need to qualify for the program. Just keep in mind these are only guidelines for qualifications. The only way to find out for sure if you can qualify for the program is to apply for an FHA loan. You'll find instructions below on how to do this.

Potential Benefits of the Program

This program offers two key benefits to home buyers: (1) smaller down payments and (2) more flexible guidelines, when compared to a conventional loan.

If you use an FHA loan to buy a house, your down payment could be as low as 3.5% of the purchase price. With a conventional mortgage, you'll have to make a larger down payment -- probably in the 5% - 10% range at a minimum.

Additionally, the guidelines for FHA approval are less stringent than those for conventional loans. This is why borrowers who have been turned down for conventional financing can often get approved through the FHA program. In many cases, these loans are the last resort for borrowers with comparatively low credit scores an/or other qualifying problems. And there is no shortage of such borrowers in the current economy.

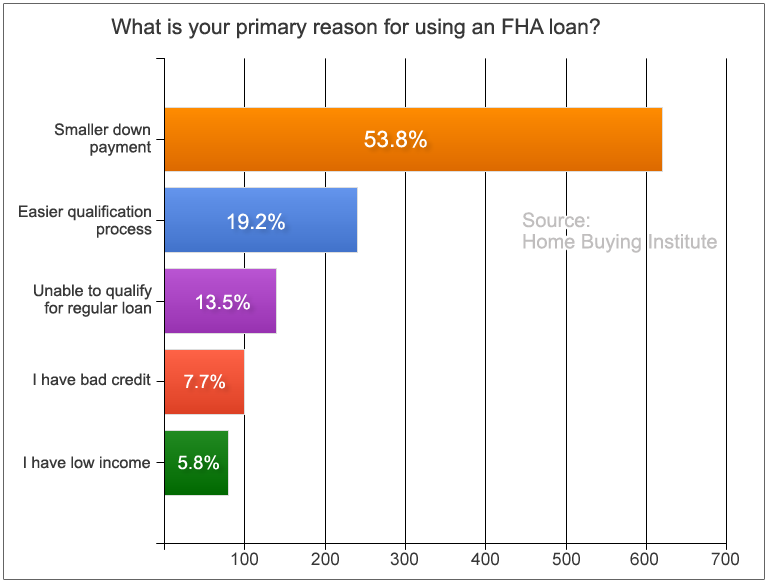

Both of these benefits attract borrowers. But it's the down-payment requirement in particular that makes the FHA loan program so popular. In 2010, we conducted a survey of home buyers to find out how many of them were planning to use the FHA program when buying a home. The vast majority said they were planning to use it. We then asked a follow-up question: What is your primary reason for using the program? Here are the results:

As you can see, the smaller down payment was by far the biggest lure for these respondents. This survey was presented to more than 12,000 future home buyers, so it's a valid indicator.

Changes to the Program: 2008 - 2012

Do a Google search for the phrase what is an FHA loan, and you'll come across a lot of conflicting information. In many cases, this is a testament to the evolving nature of the FHA program. For many years, this program was fairly 'static' in nature. It didn't change much at all. But between 2008 and 2012, there have been many changes to the program. You can probably guess why, given the 2008 start date. That's when the housing market came crashing down, resulting in a full-scale economic recession.

In the wake of this financial disaster, HUD implemented a series of changes designed to protect the FHA program and restore its depleted cash reserves.

These changes include, but are not limited to, the following:

- The down-payment requirement for FHA loans was increased to 3.5%.

- The minimum credit score needed to qualify for the 3.5% down-payment option is 580 (though many lenders still require scores of 600 or above).

- Mortgage insurance premiums (MIPs) have gone up. This includes the upfront premium as well as the annual premium.

- Borrowers must resolve any disputed items on their credit reports that exceed $1,000, before they can be approved for an FHA loan.

Again, these are not the only changes made to the program in recent years. But they are some of the most significant changes. For the latest developments in this area, check out the "In the News" section below.

How to Apply for an FHA Loan

Up to this point, we have addressed one of the two most common questions about FHA financing: What is an FHA loan? Let's move on to the second-most common question: How do I apply for one of these loans?

In order to apply for this program, you must submit an application through a lender that has been approved to participate in the program. These are referred to as FHA-approved lenders. You can find a database listing of these financial institutions on the HUD website. But you probably don't need to search their database, because almost all well-established lenders participate in the program. This includes the big banks like Wells Fargo and Bank of America, all the way down to the local banks and mortgage companies. If a company offers home loans in general, there's a 90% chance they offer FHA loans as well.

Here are the steps we recommend taking, when you apply for an FHA loan:

- Check your credit score. This is one of the key factors that will determine whether or not you get approved for the loan. It also partly determines the interest rate you receive from the lenders. It's an important three-digit number. Check your score to find out where you stand. If it's higher than 600, it shouldn't pose any qualification problems.

- Establish a budget. How much can you afford to spend each month on a mortgage payment? You should determine this number before you apply for an FHA home loan.

- Review the current average mortgage rates. You can do this by using Freddie Mac's weekly survey of the mortgage market. You won't know if you're getting a good deal from a lender unless you have some idea what the average interest rates are.

- Start gathering your paperwork. When you apply for an FHA loan, the lender will request a dizzying array of financial documents from you. If you start rounding up some of these items now, you'll have an easier time later on.

- Find an FHA-approved lender in your area. Most of the financial institutions that offer home loans participate in this program, so you shouldn't have any trouble finding one. You can use the HUD website to locate a lender, or you can use the link provided at the top of this page.

- Get pre-approved by a lender. This will give you a pretty good idea how much you can borrow -- a key piece of information for the house-hunting process. It will also help you identify any obstacles to getting the final approval. Learn more

- Shop for and find a suitable home that meets the FHA's guidelines.

- Make an offer to buy the home.

- Give your lender a copy of the purchase agreement. This needs to go into your FHA application package.

- Next comes the underwriting process, followed by the final approval (hopefully).

Obviously, this is a simplified version of events. But it does touch on the key steps in the application process. Technically, you could jump into this process at step 4 or 5. But you wouldn't have very much awareness of yourself, as a borrower, and the mortgage market in general. Steps 1 - 3 will make you a more informed applicant.

We have now addressed the two most common inquiries among home buyers: What is an FHA loan, and how do I apply for one? If you have additional questions about this subject, please refer to the list of articles in the sidebar area above.